Real Property Gains Tax Malaysia: Updated Rates, Rules & Investor Guide

Understand how real property gains tax Malaysia impacts property investors with clear guides, updated rates, and practical strategies to maximize returns while staying compliant.

Yip Tan

5/23/20268 min read

Real property gains tax can erode a profit you believed was secure. In Malaysia the tax landscape changes quickly, and a misstep can cost you dearly. KLCC Investor’s guide walks you through what the tax entails, how rates are applied, where relief may be claimed, and how to file smoothly. By the end you’ll understand the figures, key deadlines, and strategies that preserve more cash in your pocket.

Table of Contents

What Is Real Property Gains Tax in Malaysia?

How Is RPGT Calculated for Property Sales?

Exemptions and Reliefs Under RPGT

Recent Changes to RPGT Rates (2024‑2026 Update)

Common Mistakes and Penalties to Avoid

Planning Strategies to Minimise RPGT Liability

Filing RPGT: Required Forms and Deadlines

FAQ

Conclusion

What Is Real Property Gains Tax in Malaysia?

Real property gains tax, or RPGT, is a levy on the profit you make when you sell land or a building in Malaysia. The tax applies to individuals, companies and even trusts that dispose of a property. It is not a normal income tax , it only hits the gain, the difference between what you paid and what you received.

The Inland Revenue Board defines “real property” as any land situated in Malaysia and any right or interest over that land. If you own shares in a real‑property company (RPC) that meets the 75 % asset test, the sale of those shares also triggers RPGT.

Why does it matter for investors? A high‑rise condo in KLCC can double in value in a few years, but the tax bite can erode that upside. Knowing the exact rate you face helps you price a deal, decide when to hold, and plan your cash flow.

RPGT is calculated on a self‑assessment basis. Both the seller and the buyer must file a return within a set period after the Sale & Purchase Agreement (SPA) is signed. The Director General of Inland Revenue (DGIR) treats the return as the assessment itself.

For a quick snapshot, see the official schedule on the Inland Revenue Board’s website. It breaks down rates by holding period and taxpayer type.

How Is RPGT Calculated for Property Sales?

First, figure out your chargeable gain. Start with the sale price, then subtract the original purchase price, any allowable improvements, and the cost of selling (legal fees, stamp duty, agent commission). The remaining amount is your gain.

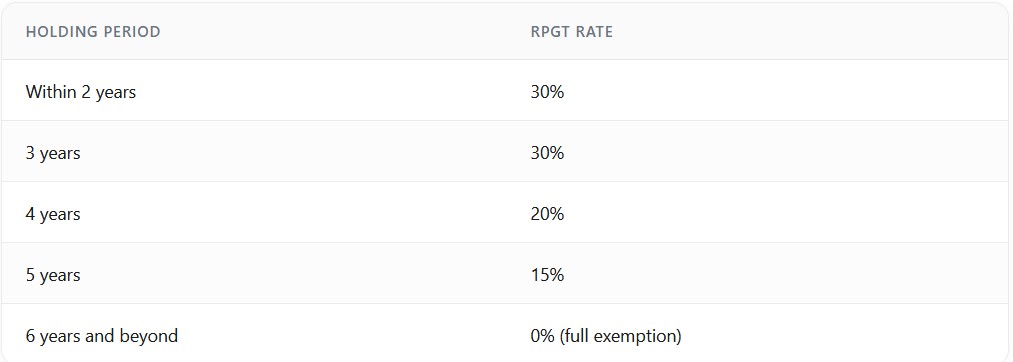

Next, apply the rate that matches your holding period. The table below shows the current rates for individual Malaysian citizens , the most common scenario for luxury buyers in KLCC.

Recent Changes to RPGT Rates (2024‑2026 Update)

The budget announced in early 2024 tweaked the rate table for non‑resident investors. While Malaysian citizens still enjoy the zero‑rate after six years, non‑residents now face a flat 30 % rate for any holding period under five years, and a reduced 15 % after five years.

In 2025 the government introduced a “luxury surcharge” on properties above RM 5 million. The surcharge adds an extra 5 % on top of the standard RPGT rate, but only for sales that occur within the first three years of ownership.

Effective 1 January 2026, the DGIR clarified the filing deadline. The deadline is now strictly 60 days from the SPA date, with a hard‑stop penalty for late filing. The earlier 90‑day grace period is gone.

These changes matter for foreign investors using the MM2H program. A non‑resident who buys a high‑end condo and flips it after two years could see a combined 35 % tax bite (30 % RPGT + 5 % luxury surcharge).

Staying current helps you decide whether to hold longer or absorb the surcharge in the purchase price.

FAQ

What is the exact holding period needed for a full RPGT exemption?

For Malaysian citizens and permanent residents, the tax drops to 0 % once you have owned the property for six years or more. The exemption applies to both residential and commercial assets, provided the sale price is above the low‑cost threshold. If you sell before the six‑year mark, you’ll face a rate that ranges from 30 % down to 15 % depending on how many years you held the property.

Do foreign investors face the same RPGT rates as locals?

No. Non‑resident buyers are taxed at a flat 30 % for disposals within five years, and 15 % thereafter. The luxury surcharge of an extra 5 % also applies to properties over RM 5 million, regardless of the buyer’s residency status.

Can I claim renovation costs as a deduction?

Yes. Costs that directly improve the property , such as structural upgrades, new fittings, or major refurbishments , are deductible. Ordinary maintenance, however, is not. Keep all invoices and receipts; the IRB may ask to see them during an audit.

What happens if I miss the 60‑day filing deadline?

The IRB imposes a 10 % penalty of the tax due for each month the return is late, up to 100 %. Interest also accrues on the unpaid tax. To avoid this, set a calendar reminder as soon as the SPA is signed and consider filing a day early.

Is there a tax credit for first‑time home buyers who sell within five years?

The IRB offers a discretionary exemption if the proceeds are used to purchase another residential property within 12 months. You must submit a written request with proof of the new purchase. The relief is not automatic; the tax officer reviews each case.

How does the Schedule 4 exemption work for low‑cost homes?

When you sell a property that cost ≤RM 200,000 and you have owned it for five years, you can claim the greater of RM 10,000 or 10 % of the chargeable gain. For example, a RM 50,000 gain yields a RM 10,000 exemption, leaving RM 40,000 taxable at the applicable rate.

Do I need to file RPGT if I sell a share in a real‑property company?

Yes. Since 1 January 2022, share disposals by individuals are subject to the same RPGT rules that applied to land sales, unless the share is held within a tax‑exempt vehicle such as a resident unit trust. The tax is calculated on the capital gain from the share sale.

Where can I find the official RPGT rate tables?

The Inland Revenue Board publishes the latest rates on its website. See the official RPGT rates page for the most up‑to‑date schedule.

Conclusion

Real property gains tax in Malaysia is a moving target, but the core principles stay the same: the tax hits the profit, the rate drops with time, and exemptions exist for long‑term owners and low‑cost homes. By calculating your chargeable gain accurately, filing within the 60‑day window, and using the holding‑period and relief strategies outlined above, you can keep more of your investment return.

We’ve covered the definition, the calculation steps, the exemptions, recent rate tweaks, common pitfalls, planning tactics and the filing process. Armed with this knowledge, you can make confident decisions about buying, holding or selling luxury KLCC assets.

Key Takeaway: RPGT only hits the profit on a property sale, and the rate depends on how long you’ve owned the asset.

Exemptions and Reliefs Under RPGT

Not every sale triggers a full‑rate charge. The law builds several reliefs that can cut the tax bill dramatically.

Full exemption applies once you hold the property for six years or more. That means if you bought a low‑cost flat for RM 180,000 and kept it for six years, the sale is tax‑free, regardless of the profit.

There is also a partial exemption for low‑cost homes (≤RM 200,000) held for five years. The Schedule 4 rule gives you the greater of RM 10,000 or 10 % of the chargeable gain. For a gain of RM 50,000, the exemption would be RM 10,000, leaving RM 40,000 taxable.

Another relief targets first‑time home buyers who sell within five years. The tax office may grant a discretionary exemption if the sale proceeds are used to buy another residential property within a set period.Corporate disposals have a different schedule. Companies face a flat 30 % rate for sales within three years, dropping to 20 % in the fourth year, and 10 % thereafter.

To claim any relief, you must file the appropriate forms and attach supporting documents , purchase agreements, renovation invoices and a declaration of intent for the first‑time buyer relief.

Key Takeaway: Extending the holding period, using low‑cost reliefs, and using corporate structures are the three levers that trim your RPGT bill.

Planning Strategies to Minimise RPGT Liability

Smart investors treat RPGT as a variable in their cash‑flow model, not an after‑thought. Below are three proven approaches.

1. Hold Past the Six‑Year Mark

If your capital allows, waiting until the property has been owned for six years wipes out the tax. The extra rental income you earn during those years often outweighs the opportunity cost of selling earlier.

Example: A luxury condo yields a 4 % net rental return. Over six years, that adds up to roughly 24 % of the original purchase price, while the tax you avoid can be as high as 30 % of the gain.

2. Use Low‑Cost Property Reliefs

For investors with a portfolio that includes affordable units (≤RM 200,000), the partial exemption can shave off 10 % of the gain. Pair this with the Schedule 4 formula to maximize the deduction.

Action step: When you buy a low‑cost unit, record the exact purchase price and keep a separate ledger for that asset. When you sell, run the Schedule 4 calculation to see whether RM 10,000 or 10 % of the gain gives you the bigger break.

3. Structure the Sale as a Share Disposal

If the property sits inside a real‑property company, selling shares instead of the land can trigger a different tax schedule. For shareholders who hold the shares for more than three years, the rate drops to 20 % and falls further after five years.

But note the 2022 amendment that moved share disposals into the broader CGT regime. Check the latest IRB circular before you use this route.

Imagine you bought a KLCC penthouse for RM 2,000,000 and sold it after three years for RM 2,800,000. Your raw gain is RM 800,000. Subtract RM 100,000 for renovation and RM 40,000 for legal fees , the chargeable gain drops to RM 660,000. At a 30 % rate, the tax owed is RM 198,000.

Pro Tip: Keep a detailed spreadsheet of purchase price, improvement costs and selling expenses. The numbers will line up when you file, and you’ll avoid over‑paying.

Common Mistakes and Penalties to Avoid

Many sellers think the tax will sort itself out. In reality, missing a deadline or filing the wrong figure can trigger steep penalties.

First mistake: waiting too long to file. The DGIR imposes a fine of 10 % of the tax due for each month the return is late, up to a maximum of 100 %.

Second mistake: forgetting to include all deductible expenses. Legal fees, stamp duty, and brokerage commissions are all allowable. Leaving them out inflates the gain and the tax.

Third mistake: assuming the buyer will withhold the correct amount. If the buyer withholds too little, you still owe the balance, plus interest.

The 2023 RPGT Guidelines, updated by a leading professional services firm, list additional penalties under Sections 29(3), 30(2) and 14(5) of the RPGTA. They include a surcharge of up to RM 5,000 for false statements, and possible criminal prosecution for deliberate fraud.

Here’s a quick checklist to keep you safe:

Mark the SPA date on your calendar and set a reminder for the 60‑day filing deadline.

Gather all invoices for improvement work, legal fees and agent commissions.

Confirm the buyer’s withholding amount before the transaction closes.

File the RPGT return using form CP2 (for individuals) or CP2A (for companies).

Keep a copy of the submitted return and the DGIR receipt for at least seven years.

Filing RPGT: Required Forms and Deadlines

When the SPA is signed, the clock starts. You have 60 days to file the RPGT return. The forms you’ll need depend on your taxpayer type.

Individuals (citizens, permanent residents): Form CP2, “Real Property Gains Tax Return”.

Companies and trusts: Form CP2A, “Real Property Gains Tax Return for Companies”.

Non‑residents: Form CP2NR, “Non‑Resident Real Property Gains Tax Return”.

Each form asks for the sale price, purchase price, improvement costs, and any exemptions claimed. Attach the following documents:

Signed Sale & Purchase Agreement.

Proof of payment for the purchase price (bank statements, receipt).

Invoices for renovations, legal fees, stamp duty, and agent commissions.

Calculation sheet showing the chargeable gain and the tax due.

Submit the completed form electronically via the IRB’s e‑LHD portal, or hand‑deliver a hard copy to the nearest IRB office. After submission, you’ll receive an acknowledgment receipt that serves as proof of filing. Remember, the buyer is required to withhold the lower of cash consideration or the self‑assessed tax amount and remit it to the DGIR within the same 60‑day window. Failure to do so can expose both parties to penalties.