Kuala Lumpur Real Estate: A Complete Guide for Buyers & Investors

Explore Kuala Lumpur real estate in 2026: market trends, property types, buying rules for foreigners, top investment zones, and renting vs buying. Get expert insights.

Yip Tan

5/15/20267 min read

Buying in Kuala Lumpur feels like stepping into a fast‑growing city where every block promises a view and a chance to grow wealth. Yet the market can feel noisy if you don’t know the basics. In this guide we break down the market, the kinds of homes you can own, the rules for foreign buyers, the hot spots to watch, and how renting measures up against buying. By the end you’ll see where the real value lives and how to act with confidence.

Table of Contents

Understanding Kuala Lumpur's Real Estate Market

Types of Properties in KL: Condos, Landed Homes, and Commercial

Can Foreigners Buy Property in Malaysia? Rules and Process

Top Areas to Invest in Kuala Lumpur: From KLCC to Mont Kiara

Renting vs Buying in KL: Which Is Right for You?

Frequently Asked Questions

Conclusion

Understanding Kuala Lumpur's Real Estate Market

Malaysia’s central position makes it a natural hub for trade, tourism, and finance. That pull fuels demand for homes, especially in the capital. Recent data shows residential prices in Greater Kuala Lumpur rose about 6% year‑over‑year, driven by strong job growth and limited land supply. Luxury homes curated by KLCC Investor illustrate how premium projects command tighter spreads and faster sales.

Why does price keep climbing? First, the city’s GDP grew 5.2% in the last year, which translates into higher rental demand as more professionals relocate for work. Second, new transit lines keep shrinking travel time, opening up suburbs that were once too far. Third, foreign investment under the MM2H scheme adds steady cash flow to the market.

According to Wikipedia’s overview of Kuala Lumpur, the metro area houses over 1.8 million people and expects to cross the 2‑million mark by 2030. More people means more need for apartments, townhouses, and office space.

JLL’s market report notes that the luxury condo segment saw a 9% price bump in the past 12 months, outpacing the broader market. The report also flags a tightening of inventory: only 2,300 units came on market versus 3,100 a year earlier. Less supply plus rising wages creates a seller’s market that can squeeze first‑time buyers.

Bottom line:Prices are climbing, inventory is tight, and demand stays strong.

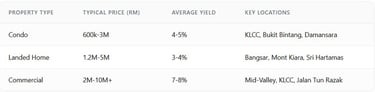

Types of Properties in KL: Condos, Landed Homes, and Commercial

When you look at listings you’ll see three main buckets: high‑rise condos, landed houses, and commercial units. Condos dominate the city centre because they fit the vertical growth model. They usually range from one‑bedroom units at RM 600,000 to penthouses north of RM 3 million.

Land‑based homes, like terrace or semi‑detached houses, sit mostly in neighborhoods such as Bangsar, Desa ParkCity, and Mont Kiara. These homes give you a garden and more privacy, but they also come with higher land taxes and longer buying cycles.

Commercial space includes office towers, retail shops, and mixed‑use developments. Investors chase these for rental yields that can reach 7‑8% in prime districts, while residential yields hover around 4‑5%.

Here’s a quick look at what each type offers:

Can Foreigners Buy Property in Malaysia? Rules and Process

Yes, foreigners can own property, but there are limits. You can buy apartments up to 30% of a development’s total floor area, and you need approval from the Economic Planning Unit (EPU). The process starts with a Letter of Intent, followed by a Sale and Purchase Agreement, then a loan‑in‑principle if you need financing.

First, check the MM2H (Malaysia My Second Home) program if you qualify. It gives you a long‑term visa and smoother financing options. KLCC Investor’s MM2H guide walks you through the paperwork step by step.

Second, secure a local lawyer. They will run a title search, ensure the developer has the proper approvals, and handle the transfer of title at the Land Office.

Third, arrange financing. Banks typically lend up to 75% of the property value for foreigners, but rates can be higher than for locals. Some lenders require a higher down‑payment if the buyer is not a resident.

Bottom line: Foreign buyers can own property and watch out for land‑type restrictions.

Top Areas to Invest in Kuala Lumpur: From KLCC to Mont Kiara

Investors chase neighborhoods that promise both rent flow and price rise. KLCC stays the crown jewel: ultra‑luxury towers, office towers, and a constant stream of expatriates. Prices here are the highest, but so are yields for short‑term rentals.

Next comes Mont Kiara, a leafy enclave favored by expatriates and high‑net‑worth families. The area blends low‑rise villas with newer condo projects, offering a stable 5‑year appreciation outlook.

Other hot spots include:

Damansara Heights , gated estates, strong capital‑gain track record.

Bangsar South , boutique condos near boutique shops.

Mid‑Valley , mixed‑use developments with strong commercial demand.

Investasian’s 2026 outlook notes that “the rise of co‑working spaces and fintech hubs pushes demand for office‑grade assets in the city centre”. That trend backs the case for buying office space in KLCC and surrounding districts.

Renting vs Buying in KL: Which Is Right for You?

Deciding whether to rent or buy hinges on cash flow, time horizon, and lifestyle. Renting gives you flexibility , you can move when your job changes or when a better condo pops up. It also means you avoid upkeep costs and property taxes.

Buying locks in a roof over your head and builds equity. If the market keeps rising, your home can become a valuable asset in five years. The flip side is you need a down‑payment, usually 20% of price, plus closing costs that can total RM 50,000‑100,000.

Let’s compare the numbers. Assume a RM 1.2 million condo. Renting a similar unit costs about RM 3,200 a month. Buying means a monthly mortgage of roughly RM 4,800 (including loan‑interest at 4.5% over 30 years). The rent‑to‑price ratio sits at 3.2%, while the mortgage‑to‑price ratio is about 4.8%.

Beyond money, think about your plans. If you expect to stay in KL for less than five years, renting usually wins. If you’re looking to build wealth and can handle the upkeep, buying lets you tap into the city’s appreciation.

Bottom line:Rent for short‑term flexibility, buy for long‑term wealth building.

Frequently Asked Questions

Can I buy a condo in KL if I’m not a Malaysian citizen?

Yes. You’ll need a local lawyer, a Letter of Intent, and a Sale and Purchase Agreement. Financing is available but often requires a larger down‑payment.

What is the Malaysia My Second Home (MM2H) program?

MM2H is a long‑term visa that lets foreigners stay in Malaysia for up to 20 years. Participants enjoy tax benefits, easier loan access, and no restriction on owning residential property, making it a popular route for high‑net‑worth investors seeking KL luxury homes.

How much cash do I need to start investing in KL?

For a mid‑range condo you’ll need roughly 20% down‑payment, which on a RM 1 million unit is RM 200,000. Add legal fees (about 1‑2% of price), stamp duty (1% for foreign buyers), and a loan‑in‑principle fee if you finance. Total cash outlay can be around RM 250,000‑300,000. For new home, developer may absorb legal fees and stamp duty which makes it more attractive and lower upfront cost.

Which area gives the best rental yields?

Commercial offices in KLCC and the Mid‑Valley corridor can reach 7‑8% yields. Among residential assets, high‑rise condos near new MRT stations, especially in Bangsar South and Damansara, typically deliver 5‑6% yields, thanks to strong expatriate demand.

Is buying through a broker better than going solo?

Working with a specialist broker like KLCC Investor gives you curated listings, market analysis, legal and financing support, and early‑access alerts via Telegram. That end‑to‑end service can shave weeks off the buying timeline and reduce hidden costs.

What taxes apply when I sell a property?

When you sell, you’ll face a real‑property gains tax (RPGT) that ranges from 0% to 30% depending on how long you held the asset. For properties held less than three years, the rate is 30%; it drops to 10% after five years. A local lawyer can help you plan to minimize the tax impact.

How does the new MRT line affect property values?

Transit upgrades cut commute times, making previously out‑of‑reach neighborhoods attractive. Historical data shows that properties within a 500‑meter radius of a new MRT station can see price jumps of 8‑12% within two years after opening.

Can I use a foreign loan to buy in KL?

Some international banks offer cross‑border mortgages, but they often come with higher interest rates and stricter underwriting. Most buyers prefer a Malaysian bank loan, which can fund up to 75% of the price for foreigners, especially if you have an MM2H visa.

Conclusion

Kuala Lumpur’s real‑estate market offers a mix of growth, liquidity, and prestige. Whether you chase high‑rise condo appreciation in KLCC, steady expat demand in Mont Kiara, or solid office yields in the Mid‑Valley, the city’s fundamentals support long‑term upside. We’ve laid out the market forces, property types, foreign‑buyer rules, top districts, and the rent‑vs‑buy calculus you need to decide.

Now that you know the landscape, the next step is to act with data‑driven confidence. KLCC Investor delivers curated listings, market analysis, legal and financing help, plus real‑time Telegram alerts that let you jump on premium units before they hit the public market. Ready to secure a luxury address that’s more than a property , it’s a statement of growth and prestige? Start your free trial today and let us guide you from search to settlement.

Key Takeaway: Kuala Lumpur’s real‑estate market is on an upward swing, powered by strong GDP, transit upgrades, and foreign buyer interest.

Key Takeaway: "The best way to capture KL’s upside is to own where the city’s elite live and work."

KLCC offers prestige and liquidity; Mont Kiara offers steady growth and expat demand.

Pro Tip: If you aim for capital growth, focus on condos near new MRT stations; they tend to appreciate faster than older landed homes.

Pro Tip: Run a simple rent‑vs‑buy calculator: multiply monthly rent by 12, then compare to annual mortgage payments plus taxes. If the rent cost is less than 30% of the purchase price, renting often makes financial sense.