Home Loan Malaysia – Best Financing Options for Property Buyers

Explore top home loan providers in Malaysia, compare rates, features and eligibility to find the right financing for your property. Choosing the right home loan Malaysia package is crucial for buyers who want competitive interest rates and long‑term financial stability.

Yip Tan

5/17/20268 min read

Malaysia’s property market can be financed at a jaw‑dropping 2.88%, a rate that shatters the 4%‑plus average most buyers expect. You’re probably hunting for a loan that won’t bleed your cash flow and still lets you snap up a premium condo in KL. In this list we break down the top eight lenders, flag the quirks that matter, and give you a quick checklist so you can pick the right fit for your lifestyle and investment goals.

Table of Contents

1. Maybank Home Loan, Low Interest for First‑Time Buyers

2. CIMB Home Loan, Flexible Repayment Options

3. Public Bank Housing Loan, Fast Approval Process

4. Hong Leong Bank Home Loan, Competitive Rates for High‑Value Properties

5. RHB Home Loan, No Early Settlement Fees

6. Bank Islam Home Financing, Sharia‑Compliant Financing

7. What to Look for When Choosing a Home Loan in Malaysia

8. Home Loan Malaysia Comparison Table

FAQ

Conclusion

1. Maybank Home Loan, Low Interest for First‑Time Buyers

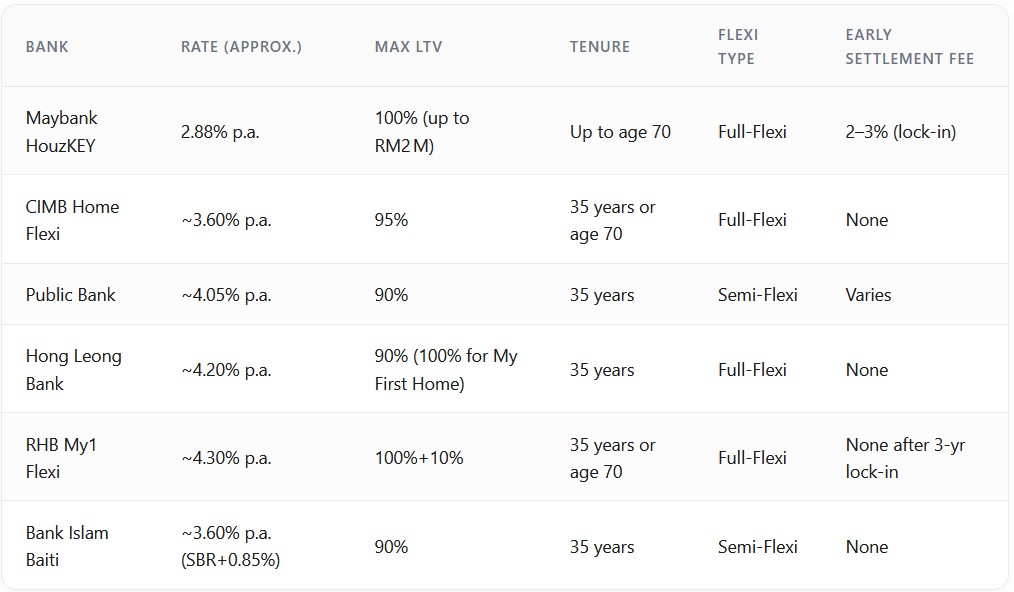

Maybank’s HouzKEY package has been quoted at 2.88% p.a., the lowest rate we’ve seen for a luxury purchase. That figure comes from the Standardised Base Rate (SBR) of 2.75% plus a tiny spread. For a RM500,000 loan over 30 years, the monthly payment drops by about RM413 compared with a 4.35% loan, saving roughly RM149,000 in total interest

Here’s what you get:

Up to 100% financing for properties under RM2 million (rare in the market).

Fixed profit‑rate segment for the first 5 years, giving payment certainty.

Zero‑moving‑cost package that can absorb legal, valuation and stamp‑duty fees.

But the low rate comes with a 3‑5‑year lock‑in. If you settle early, you’ll face a 2, 3% penalty on the outstanding balance. That’s why you should be sure you’ll stay put for at least that long.

Bottom line: Maybank is the go‑to for first‑time buyers who value a rock‑bottom rate and can commit to the lock‑in period.

2. CIMB Home Loan, Flexible Repayment Options

CIMB’s Home Flexi product blends a loan with a linked current account. Every ringgit you keep in the account automatically offsets your loan balance, cutting interest day‑by‑day. You can deposit, withdraw, or transfer funds through the CIMB Octo App, so cash flow stays fluid.

Key features include:

Financing up to 95% of the property price, inclusive of MRTA, MLTA and legal fees (capped at 5%).

Tenure up to 35 years or age 70, whichever comes first.

Full‑flexi structure , excess payments reduce principal instantly, and you can pull the money back without a fee.

Imagine you have RM20,000 spare each month. You park it in the linked account; the bank deducts interest on the lower balance, saving you a few hundred ringgit each year.

Pro Tip: Use the linked account as an emergency buffer. Keep a few months of expenses there; you’ll still cut interest while having instant access.

For investors who like to juggle cash, the flexibility is a huge win. Just watch out for a modest monthly management fee on the current account.

Bottom line: CIMB’s Flexi loan is ideal for borrowers who want a dynamic way to reduce interest while keeping liquidity.

3. Public Bank Housing Loan, Fast Approval Process

Public Bank is known for a simplifyd document submission system. Once you upload the required income proofs, the bank can issue a conditional approval in as little as 48 hours. That speed can be a game‑changer in a hot market where properties sell within days.

Features include:

Margin of financing up to 90% for most residential units.

Tenure options from 5 to 35 years.

Fast‑track processing for salaried employees and government staff.

Here’s a quick look at the flow:

Submit income documents via the online portal.

Bank runs a CCRIS check and calculates your Debt Service Ratio.

Receive a conditional offer within two days.

The downside? Public Bank doesn’t offer the same level of fee‑absorption as some rivals, so you’ll need to budget for legal and valuation costs.

Bottom line: Choose Public Bank if you need a rapid approval and are comfortable handling standard fees yourself.

4. Hong Leong Bank Home Loan, Competitive Rates for High‑Value Properties

Hong Leong targets buyers of premium units with a rate that sits just under the market median. The bank lets you make extra payments of any amount at any time, and interest is calculated daily , a tiny edge that adds up over a long tenure.

Highlights:

Margin of financing up to 90%, with a special 100% scheme for first‑time buyers under the My First Home program.

Daily interest calculation means every extra ringgit you pay cuts the balance faster.

Processing fee of RM0.50 per cheque , a nominal charge for large‑value deals.

Because the bank focuses on high‑value properties, you’ll often see lower spreads for loans above RM400,000. That makes it a solid pick for luxury investors who plan to hold the asset for a decade or more.

One thing to watch: the bank’s tenure caps at age 70, so older borrowers should calculate the effective loan length early.

Bottom line: Hong Leong offers a balanced mix of competitive rates and flexibility for high‑value homes.

FAQ

What is the typical margin of financing for a luxury home in Malaysia?

Most banks finance between 85% and 90% of the property price. Maybank’s HouzKEY can go up to 100% for qualifying projects, which is an outlier that helps high‑net‑worth buyers keep cash on hand for other investments.

How does a full‑flexi loan differ from a semi‑flexi loan?

Full‑flexi loans link a current account to the loan, so any extra cash you deposit instantly reduces the principal and interest. Semi‑flexi loans let you make extra payments that cut principal, but you usually need to request a withdrawal and may pay a small fee.

Can I get a home loan as a foreigner under the MM2H program?

Yes. CIMB and a few other banks offer dedicated MM2H packages with up to 85% LTV. These loans often come with flexible documentation requirements, making it easier for non‑resident buyers to secure financing.

What are the typical fees I should budget for besides the interest rate?

Expect legal fees, valuation fees, stamp duty, and possibly a processing fee per cheque (e.g., RM0.50 at Hong Leong). Some banks bundle these into a zero‑cost package, which can save you several thousand ringgit upfront.

How does the lock‑in period affect my ability to refinance?

During the lock‑in (usually 2, 5 years) you’ll pay a penalty of 2, 5% of the outstanding loan if you refinance early. After the lock‑in ends, you can refinance without penalty, which is why many borrowers wait until the period expires before switching to a lower‑rate product.

Is a Sharia‑compliant home financing more expensive than a conventional loan?

The profit rate is often comparable to the spread on a conventional loan. However, the structure can lead to slightly higher total cost if the markup is fixed and the market rate drops later. For many, the ethical advantage outweighs the minor cost difference.

What documentation do I need to prepare for a home loan application?

You’ll need proof of identity, income (salary slips or tax returns), bank statements, a property valuation report.

Should I choose a fixed‑rate or variable‑rate loan for a luxury condo?

Fixed rates give payment certainty but are usually higher at the start. Variable rates track the SBR and can be cheaper if the OPR stays low. For a long‑term hold, a variable rate with a full‑flexi structure often wins on total interest saved.

Conclusion

We’ve laid out the top home loan picks for Malaysia’s high‑end market. Maybank shines with the lowest headline rate, CIMB offers unmatched flexibility, Public Bank speeds up approval, Hong Leong balances rate and extra‑payment freedom, RHB eliminates early‑settlement penalties, and Bank Islam delivers Sharia‑compliant options. The right loan depends on what you value most , pure rate, cash‑flow agility, quick approval, or ethical financing.

At KLCC Investor we back luxury buyers with data‑driven market insights, legal support, and a free loan‑comparison tool that pulls the latest rates into one view. Start your free loan assessment today and lock in the financing that matches your prestige and growth goals.

Key Takeaway: Maybank offers the lowest headline rate, but the lock‑in period can add hidden costs if you move early.

"Speed matters when you’re bidding on a prime KL condo , a delay can cost you the deal."

Pro Tip: Use the linked account as an emergency buffer. Keep a few months of expenses there; you’ll still cut interest while having instant access.

Pro Tip: Use RHB’s calculator to run a break‑even analysis before you decide to refinance.

5. RHB Home Loan, No Early Settlement Fees

RHB’s My1 Flexi package lets you pay extra whenever you like, and you can even pull those extra payments back without a steep penalty. The bank also waives early settlement fees, which is rare in the Malaysian market.

Key points:

Financing up to 100% + 10% (including MRTA/CLTA and FEC) for eligible projects.

Lock‑in period of 3 years, but no penalty if you settle early after that.

Online loan calculator helps you model repayments instantly.

Imagine you refinance a RM600,000 loan after five years. With RHB you can settle without paying the typical 2% penalty, saving you tens of thousands of ringgit.

The only drawback is a slightly higher spread than the market’s lowest rates, but the fee‑free early settlement can outweigh that for many investors.

Bottom line: RHB is perfect for borrowers who value flexibility and want to avoid early‑settlement penalti

6. Bank Islam Home Financing , Sharia‑Compliant Financing

Bank Islam’s Baiti Home Financing‑i follows the Murabaha model: the bank buys the property, then sells it to you at a markup, which you repay in instalments. The profit rate currently sits at SBR + 0.85%, translating to roughly 3.60% p.a. for qualified buyers.

Benefits include:

Fully Sharia‑compliant, no interest, only a transparent profit margin.

Financing up to 90% of the property value, with the option to add MRTA and legal fees.

Available to both Muslim and non‑Muslim borrowers, expanding the pool of eligible investors.

Because the profit rate is fixed for the early years, you get payment certainty even if the Base Rate shifts later. That can be a relief for expats using the MM2H program who prefer predictable cash flow.

Do note that the contract requires a full‑payment of the markup upfront, so the total cost can be slightly higher than a conventional loan with the same headline rate.

Bottom line: Bank Islam is the top choice for buyers who need Sharia‑compliant financing without sacrificing flexibility.

Pro Tip: Pair the Baiti loan with Bank Islam’s Takaful mortgage protection to guard against job loss or disability.

7. What to Look for When Choosing a Home Loan in Malaysia

Picking a loan isn’t just about the headline rate. You need to weigh the whole package: margin of financing, tenure, fees, lock‑in period, and any special perks that match your cash flow.

Here are the five pillars you should rank:

Interest rate & spread: Even a 0.25% gap can mean tens of thousands saved over 30 years.

Margin of financing (MOF): Higher MOF means lower down‑payment, but it can raise the bank’s risk and affect the spread.

Flexibility: Full‑flexi or semi‑flexi loans let you make extra payments that cut interest.

Fees & penalties: Look for early‑settlement fees, processing fees, and lock‑in penalties.

Additional perks: Zero‑cost moving packages, cashback, or bundled insurance can tip the scales.

For luxury buyers, the extra perks often outweigh a few basis‑points difference in rate. That’s why we see many investors choose full‑flexi loans even when the spread is marginally higher.

We also recommend checking the latest SBR figure, which the central bank updates after each OPR move. Bank Negara Malaysia publishes the current rate, and you can use it to gauge how much a variable loan might swing.

Bottom line: Evaluate the full cost structure and flexibility, not just the headline rate, to pick the best home loan for your luxury purchase.

"A low rate is great, but a loan that lets you pay extra without penalty is priceless for an investor."

8. Home Loan Malaysia Comparison Table